As of March 2025, India had 18,318 classified wilful defaulters, collectively owing ₹3,83,264 crore to the Indian banking system, source: The New Indian Express. That is not a historical relic. Those are active individuals and entities, identified and listed, who are legally prohibited from receiving new credit from any lender in India.

Now here is the question that should follow immediately: how many of them have tried to re-enter anyway?

The honest answer is that no institution can say with confidence, because most lending systems do not have the infrastructure to detect it.

Key Takeaways

- ₹3.83 lakh crore is owed by 18,318 wilful defaulters in India: individuals legally barred from new credit who remain active and motivated to find ways back into the lending system.

- RBI’s July 2024 Master Direction is unambiguous: no additional credit facility shall be granted to a wilful defaulter or any entity with which they are associated. The obligation is the lender’s, not just the borrower’s.

- Re-entry happens through four primary routes: name and detail modification, fresh identity documents, using associates or entities, and targeting NBFCs and digital lenders with less stringent cross-checking.

- The NPA photo and field repository is the detection infrastructure: without a searchable historical database of defaulter photographs and identity fields, the prohibition exists on paper but not in practice.

- Face matching catches the defaulter who changes their name: the photograph is the constant; AI matches it against the repository regardless of what name appears on the new application.

- OCR field cross-check catches the defaulter who changes their photograph: reused PAN, address, mobile, or employer ID is flagged even when the face is different.

- Detection must happen at origination: a wilful defaulter who successfully obtains a new loan represents a compounding loss: the original NPA plus the fresh disbursement.

The Re-Entry Problem Nobody Talks About

India’s NPA story over the last five years has largely been a recovery story. The gross NPA ratio of scheduled commercial banks dropped to a multi-decade low of 2.15% by September 2025, per RBI’s Report on Trend and Progress of Banking in India 2024-25. source: PIB The headline numbers reflect genuine improvement, better credit assessment, IBC enforcement, SARFAESI action, improved provisioning discipline.

But here is what the headline NPA ratio does not tell you: what happens at the other end of the cycle, when a known defaulter attempts to re-enter the lending system under a modified or new identity.

In December 2025, UP’s Special Task Force busted a ₹100-crore fraud ring operating out of Noida, a syndicate that had been systematically using forged Aadhaar, PAN, and identity documents to create fake profiles and obtain loans from at least 10 banks, source: Times of India. Among the material recovered: digital printers, laptops, and specialised forgery software. The gang had been running for several years. Their core method was creating new financial identities for individuals who could not borrow under their real ones.

The regulatory framework is clear about what should happen. RBI’s July 2024 Master Direction on Wilful Defaulters states explicitly: no additional credit facility shall be granted by any lender to a wilful defaulter or any entity with which a wilful defaulter is associated. The prohibition is absolute. The enforcement gap is not in the rule; it is in the detection.

A rule that says a defaulter cannot borrow again is only as strong as the lender’s ability to recognise the defaulter when they walk back in.

Four Routes Defaulters Use to Re-Enter

Understanding how re-entry actually happens is the starting point for building detection that stops it.

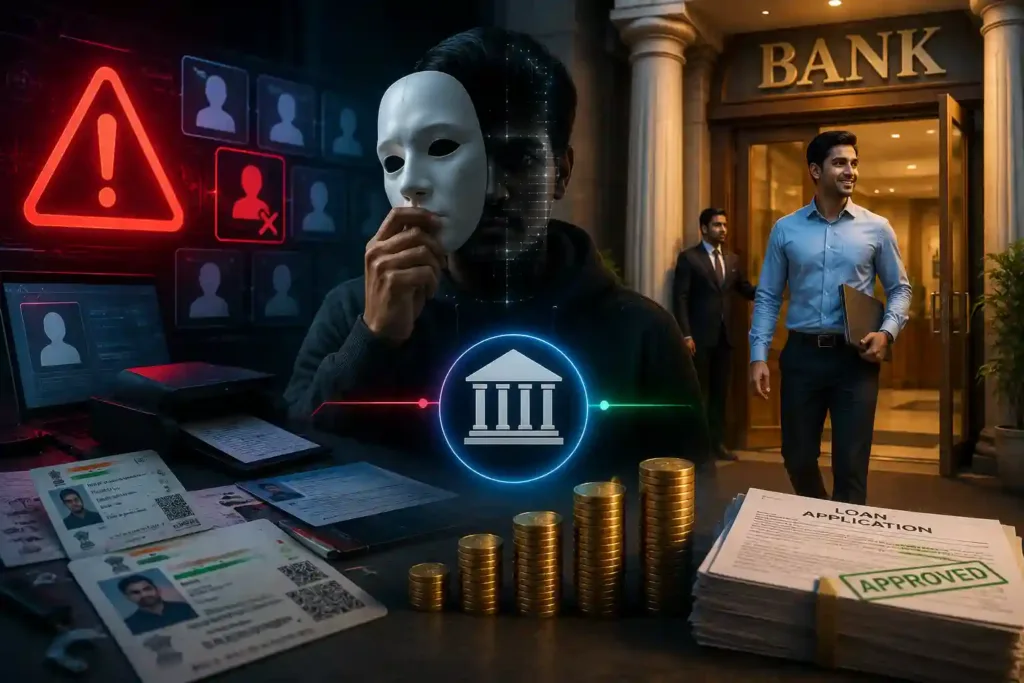

Route 1: Name and detail modification

The simplest approach. Change the spelling of the name: Suresh Gupta becomes S. Gupta becomes Suresh K. Gupta. Change the registered mobile number. Use a different address. Keep the same photograph, the same PAN, the same fundamental identity, but modify enough surface details that a manual check against a defaulter list does not return a match. This works because most defaulter checks are text-based, matching names and identifiers against listed records. Name variants and abbreviations defeat text matching. They do not defeat photo matching.

Route 2: Fabricated or borrowed identity documents

More sophisticated. Obtain forged Aadhaar and PAN documents under a different identity, either entirely fabricated or using documents belonging to another real person. Submit an application that, on paper, belongs to someone who has no prior lending history. This route is what the Noida STF case documented: organised operations that specifically manufacture clean identities for people who cannot borrow under their own.

Route 3: Using associated entities

RBI’s Master Direction specifically extends the prohibition to entities associated with the wilful defaulter, directors, promoters, and group companies. A defaulter who cannot borrow personally may attempt to borrow through a newly incorporated company, a spouse’s name, or an associate. Detection requires entity-level association analysis beyond the individual applicant.

Route 4: Targeting lenders with weaker cross-checking

An NBFC or digital lender with less robust historical data and weaker identity verification is a more attractive target than a large bank with mature fraud systems. Experienced defaulters, and the organised operators who help them, actively identify the channels of least resistance. This is a structural risk as lending continues to expand through digital and NBFC channels.

Why Current Systems Miss Re-Entry

Most lending institutions have some form of defaulter check at origination, a query against CIBIL, a check against the RBI’s wilful defaulter list published on CIBIL’s platform, an internal blacklist search. These checks are valuable. They are not sufficient.

Text-based checks are defeated by name variants

A CIBIL check on “Suresh Kumar” will not surface “S.K. Verma”, even if the underlying individual is identical. Name-matching systems that use exact or near-exact string comparison cannot reliably catch the deliberate name modifications that experienced defaulters use.

CIBIL wilful defaulter lists cover classified wilful defaulters

Not the broader universe of NPA accounts, written-off borrowers, and fraud-tagged accounts that also represent high re-entry risk. A borrower whose account was written off but who was not formally classified as a wilful defaulter may not appear on the CIBIL list, but still represents a borrower whose credit history should prevent new disbursement.

Cross-institution information lags

NPA classification and wilful defaulter reporting have defined timelines. A borrower who defaulted recently and whose account has not yet been formally classified and reported may be invisible to an originating lender’s external data checks.

Fabricated documents defeat document-based checks

If the identity documents submitted are forged, a check against the identity on those documents returns nothing, because the fraudulent identity has no prior history. The detection must go deeper than the document to the face and the fields behind it.

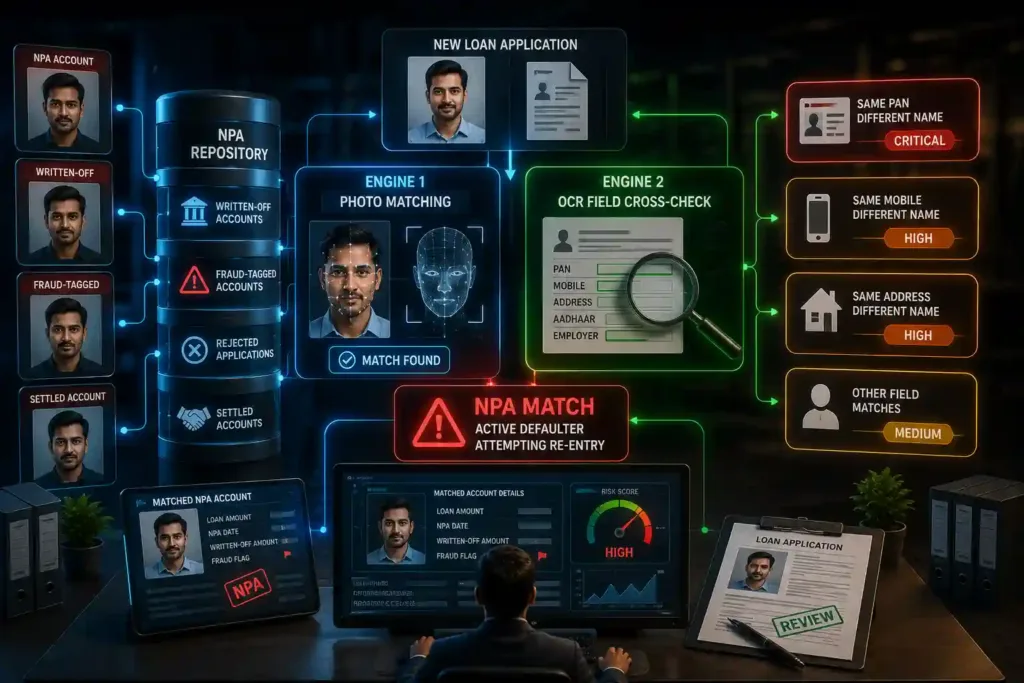

How AI-Powered NPA Match Detection Works

The detection architecture that closes the re-entry gap operates across two parallel engines, the same dual-engine approach used for identity reuse detection, but sourced from a different and specifically NPA-focused repository.

The NPA Photo and Field Repository

The foundation of effective NPA match detection is a maintained, searchable repository that goes beyond the CIBIL wilful defaulter list to include:

Written-off and NPA loan accounts

Every account that was declared NPA and subsequently written off. The borrower may not be formally classified as a wilful defaulter, but their history makes them a high re-entry risk.

Fraud-tagged accounts

Accounts where fraud was identified at any point in the loan lifecycle, regardless of whether the borrower was classified as a wilful defaulter.

Rejected applications with fraud indicators

Applicants rejected previously for fraud-related reasons, including forged documents or inconsistent identity fields.

Settled accounts under structured arrangements

Borrowers who settled for less than the outstanding amount, particularly under OTS (One Time Settlement) arrangements, represent a risk profile that warrants additional scrutiny on reapplication.

Every account in this repository contributes a photograph and a set of identity fields, name, mobile number, PAN, Aadhaar hash, address, employer. Together they form the detection database that makes re-entry identification possible.

Engine 1: Photo Matching Against the NPA Repository

When a new loan application is received, the submitted photograph is processed through the face embedding engine. The resulting facial vector is compared against the full NPA repository, not just the active loan files and rejected applications, but specifically the NPA, written-off, and fraud-tagged accounts.

A match above the confidence threshold generates a specific alert type: NPA Match, active defaulter attempting re-entry.

The alert includes the matched account details, the original loan amount, the NPA classification date, the written-off amount if applicable, the fraud flag if present. The originating loan officer and fraud team immediately see not just that there is a match, but the full context of what that match represents.

This catches Route 1 and Route 2 re-entry, the defaulter who modifies their name and the defaulter who change surface identity details, because the face comparison is indifferent to what name appears on the form.

For how photo matching works at the technical level, read: Identity Reuse Fraud in Loan Applications →

Engine 2: OCR Field Cross-Check Against NPA Records

In parallel, the OCR document intelligence engine extracts all identity fields from the submitted application and documents and cross-references them against the NPA repository field index.

A defaulter who successfully obtains a different photograph, whether through a different photo taken at a different time or through document forgery, may still reuse their actual PAN number (because they need it for income tax purposes), their actual mobile number (because they need to receive disbursement communications), or their actual address (because they have no alternative).

Each of these reused fields generates a specific alert:

Same PAN, different name: CRITICAL. A PAN number that exists in the NPA repository under a different name is a direct re-entry signal.

Same mobile, different name: HIGH. The mobile number registered in the NPA account reappearing under a different named applicant.

Same address, different name: HIGH. The residential address from the NPA account appearing on a new application under a different name.

The combination of photo matching and field cross-check creates overlapping detection nets; a defaulter who slips through one faces the other.

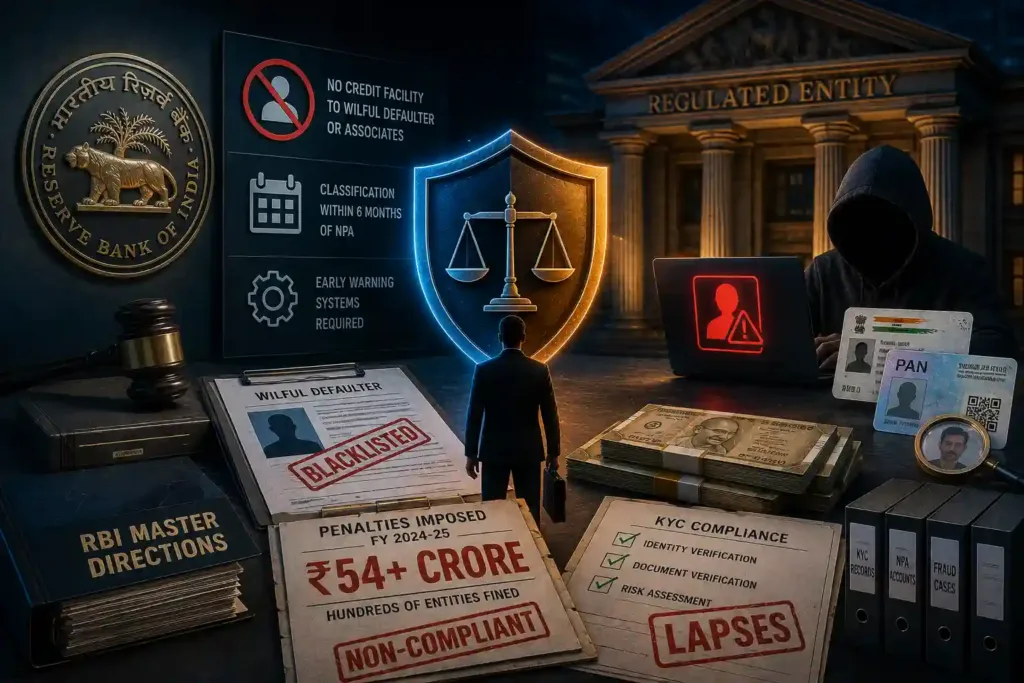

What RBI Requires, And Why This is a Compliance Obligation, Not Just a Risk Decision

This is not discretionary best practice. The regulatory framework creates a clear obligation.

RBI’s July 2024 Master Direction on Wilful Defaulters mandates that no lender shall grant additional credit facilities to a wilful defaulter or any entity with which a wilful defaulter is associated. The lenders are required to examine the wilful default aspect in all NPA accounts with outstanding amounts of ₹25 lakh and above. The wilful defaulter classification process must be completed within six months of the account being classified as NPA.

RBI’s Fraud Risk Management Master Directions (July 2024) require Early Warning Systems integrated with Core Banking Solutions, proactive systems that identify fraud risk at origination, not retrospectively.

In FY 2024-25 alone, RBI imposed over ₹54 crore in penalties across hundreds of regulated entities for KYC lapses. Banks including large private sector institutions faced multi-crore fines for failures in their onboarding processes.

Disbursing a loan to a known wilful defaulter, or to someone presenting a modified identity that the institution had the technical means to identify as a defaulter, is not just a credit loss. It is a potential regulatory finding. The obligation to detect is explicit. The question is whether the infrastructure to fulfil that obligation is in place.

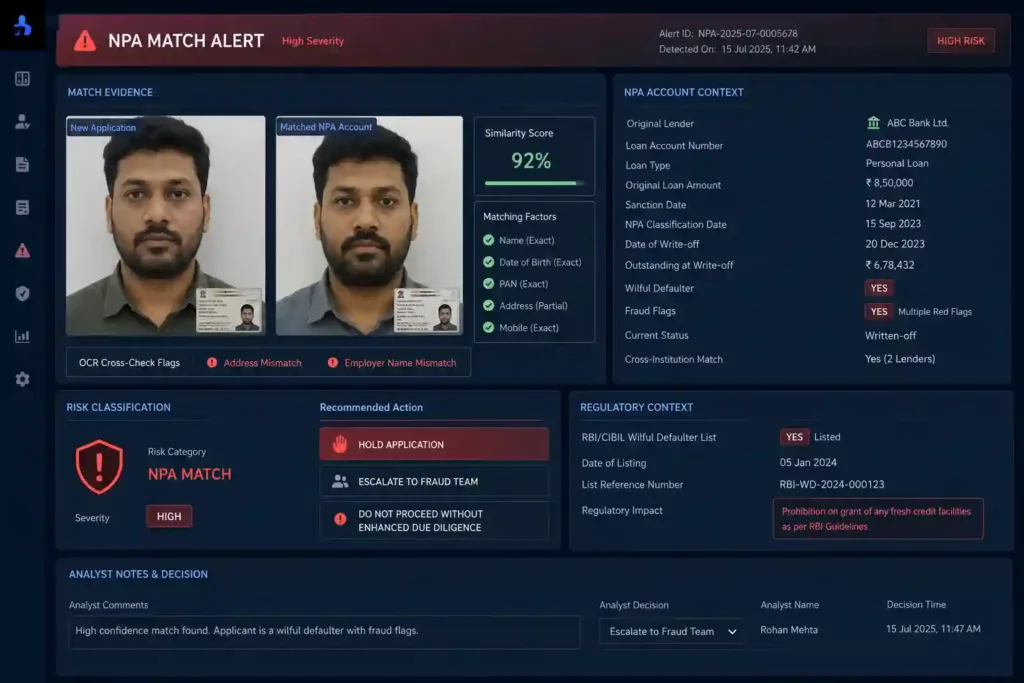

What the Alert Looks Like in Practice

When the NPA match detection system flags a re-entry attempt, the alert presented to the analyst contains:

The match evidence

Side-by-side photographs, new application and matched NPA account. Similarity score. The specific fields that triggered OCR cross-check flags if applicable.

The NPA account context

Original loan amount. Date of NPA classification. Outstanding at write-off. Whether the account was formally classified as a wilful defaulter. Any fraud flags on the account. The lender that originated the original loan (for cross-institution matching if applicable).

The risk classification

NPA Match alert, severity level, recommended action, hold application, escalate to fraud team, do not proceed without enhanced due diligence.

The regulatory context

Whether the matched defaulter is on the RBI/CIBIL wilful defaulter list, relevant for the mandatory prohibition on new credit facilities.

The analyst’s decision is informed by the complete picture, not just a name-match flag.

Frequently Asked Questions

1. What is NPA match detection in loan origination?

NPA match detection is the process of comparing a new loan applicant’s photograph and identity fields against a maintained repository of existing NPA accounts, written-off loans, fraud-tagged accounts, and classified wilful defaulters, identifying re-entry attempts by known defaulters before any disbursement decision is made. It combines AI-powered facial recognition with OCR document field cross-referencing to catch both straightforward re-entry and attempts to evade detection through name modification or partial identity changes.

2. How many wilful defaulters are there in India?

As of March 2024, approximately 2,664 borrowers had been classified as wilful defaulters in India, collectively owing ₹1.94 lakh crore to the banking system, per RBI data. This figure covers only those formally classified under RBI’s wilful defaulter framework, the broader universe of NPA accounts, written-off borrowers, and fraud-tagged accounts represents a significantly larger population of individuals with high re-entry risk.

3. Are wilful defaulters legally prohibited from getting new loans?

Yes. RBI’s July 2024 Master Direction on Wilful Defaulters explicitly prohibits any lender from granting additional credit facilities to a classified wilful defaulter or any entity with which a wilful defaulter is associated. The prohibition covers all regulated lenders, banks, NBFCs, housing finance companies. The challenge is detection: the prohibition exists in regulation; enforcing it requires the ability to identify the defaulter when they apply under a modified or different identity.

4. Can a wilful defaulter apply for a loan using a different name?

They can attempt to. Name modification, using variants, abbreviations, or entirely different names supported by forged documents, is one of the primary routes through which known defaulters attempt to re-enter the lending system. Text-based defaulter checks are vulnerable to name variants. AI-powered photo matching, which compares facial embeddings rather than name strings, detects the same person regardless of the name on the application.

5. What is the difference between an NPA and a wilful defaulter?

An NPA (Non-Performing Asset) is any loan where principal or interest payments have been overdue for more than 90 days, it may arise from genuine financial hardship as much as deliberate non-payment. A wilful defaulter is a specific classification for borrowers who had the capacity to repay but deliberately chose not to, including cases of fund diversion, asset disposal, or deliberate evasion. All wilful defaulters are NPAs, but not all NPAs are wilful defaulters. Both categories represent re-entry risk and should be included in the NPA match detection repository.

6. Does NPA match detection work for digital and app-based loan applications?

Yes, and it is particularly important for digital channels precisely because they lack the face-to-face verification that branch-based origination provides. A defaulter applying through a mobile app or DSA channel faces no human check of any kind at origination. An automated NPA photo matching system that runs on every digital application, regardless of channel, provides the same detection capability across all origination channels simultaneously.

Also read:

For the complete picture of loan fraud typologies and how the detection stack works, read: Loan Fraud Detection: The Complete Guide for Banks and NBFCs in India →

For how mule accounts connect to defaulter re-entry operations, read: Mule Account Detection →