In a documented enforcement case, the Enforcement Directorate arrested two chartered accountants and a cryptocurrency trader for a financial fraud totalling ₹640 crore. The money hadn’t moved in a straight line. It had passed through thousands of mule bank accounts before being converted into cryptocurrency, each account a separate transaction, each hop a deliberate attempt to obscure the origin of the funds.

That is the money laundering problem in its modern form. Not a simple transfer from one place to another, but a deliberate architecture of complexity, accounts, entities, jurisdictions, and instruments layered on top of each other until the original crime is invisible to any investigator who has to trace the trail by hand.

The UNODC estimates that between 2% and 5% of global GDP, up to $2 trillion, is laundered each year. Only 1% of those illicit financial flows are detected and seized. That gap is not primarily a legal problem or a regulatory problem. It is an investigative capacity problem. And it is exactly where AI-powered money trail analysis has the most to offer.

India’s AML Enforcement Is Accelerating, The Data Demand Is Too

India’s enforcement posture has shifted significantly. The Enforcement Directorate attached assets worth ₹81,422.63 crore in FY 2025–26 alone, more than fifteen times the cumulative attachment value recorded in the first decade of PMLA enforcement between 2005 and 2014. The ED’s own annual report for FY 2025–26 explicitly identifies technology-driven enforcement and AI-powered systems as the direction of its investigative strategy going forward.

The numbers behind that trajectory matter. The Finance Minister reported to the Rajya Sabha that 5,892 PMLA cases have been registered since 2015. The conviction figure stands at 15. That is not a criticism of the investigating institutions, it is a reflection of how difficult money laundering cases are to build to the standard of proof a court requires, when the evidence is spread across hundreds of entities, multiple jurisdictions, and instruments that were chosen specifically to resist tracing.

The implication is direct: investigation volume is increasing, case complexity is increasing, and the evidentiary standard required for conviction demands more thorough money trail documentation, not less. This is the environment in which automated money trail analysis becomes operationally urgent, not as a replacement for investigative judgement, but as the capability layer that makes comprehensive tracing achievable at the scale the enforcement agenda now requires.

Where the Trail Gets Complicated: The Layering Stage

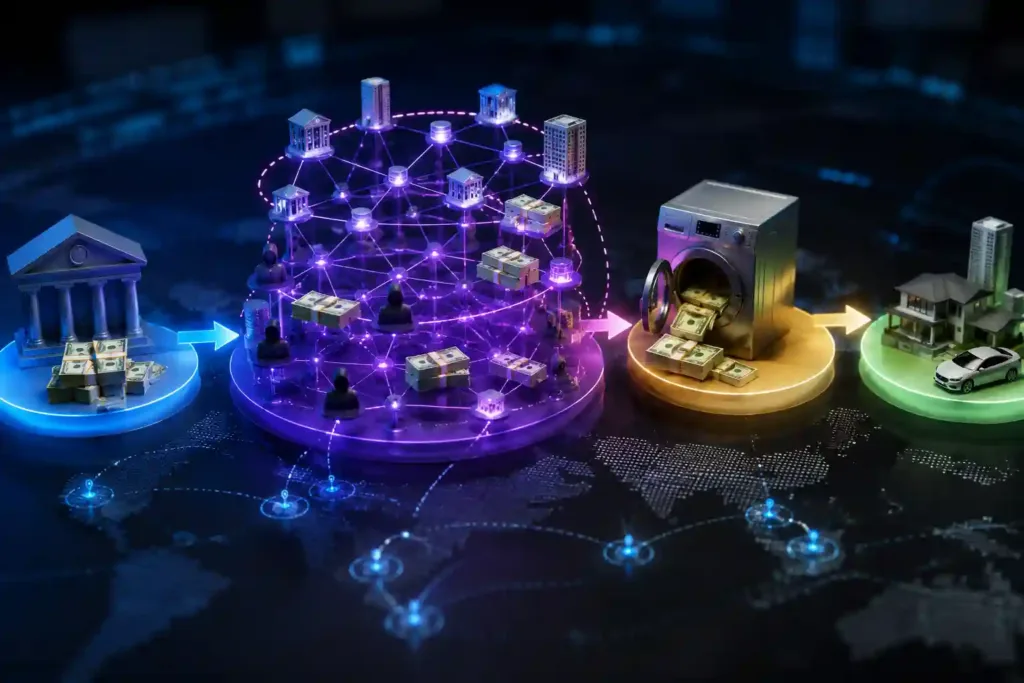

Money laundering moves through three stages: placement, where illicit funds enter the financial system; layering, where those funds are moved through complex transactions to obscure their origin; and integration, where the cleaned money re-enters the economy as legitimate assets.

The placement stage is increasingly well-monitored. STR (Suspicious Transaction Report) reporting by banks, transaction monitoring systems, and cash threshold rules have made the entry point more visible than it has ever been. The integration stage, real estate, business investment, asset acquisition, leaves paper trails that investigators can follow once a case is open.

The layering stage is where investigation gets genuinely hard. This is where funds move through multiple bank accounts, across multiple entities, sometimes across multiple jurisdictions, in patterns deliberately designed to be complex. Mule accounts change hands. Shell companies pass funds through legitimate-looking intermediaries. Informal channels, hawala networks, cryptocurrency, move value outside the formal financial system entirely.

Tracing this manually, across thousands of transactions and dozens of entities, is the core investigation challenge. It is time-intensive, it scales poorly, and the connections that matter most, the ones that reveal the beneficial owner or the source of funds, are often the ones most deeply buried in the complexity.

This is where AI-powered automation changes the equation.

What AI Can Do for Money Trail Analysis

Entity Relationship Mapping at Transaction Scale

The first and most immediate contribution of AI in money trail investigation is the automatic construction of an entity relationship map from transaction data.

Instead of an investigator manually tracing each hop, account A transferred to account B, which transferred to accounts C, D, and E, each of which connected to five further accounts, an AI agent processes the full transaction dataset and renders the complete network graph automatically. Every entity, every connection, every flow of funds is visible simultaneously, rather than assembled step-by-step over days of manual work.

The graph does more than show connections. It reveals structure. Accounts that appear as nodes with many connections to otherwise unrelated entities flag themselves as potential aggregation or distribution points in the laundering network. Entities that appear in multiple separate transaction clusters, separated by time, surface as the connective tissue linking ostensibly unrelated activity. These structural signals are what an experienced financial investigator looks for instinctively, and what an AI system can surface automatically, across datasets too large for instinct to cover.

Cross-Jurisdiction Transaction Tracing

Money laundering frequently exploits the seams between financial systems, domestic banks to foreign accounts, regulated institutions to jurisdictions with weaker AML frameworks, formal banking to informal transfer mechanisms.

Cross-jurisdiction tracing is where manual investigation hits its hardest limits. Requesting records from foreign financial institutions through formal channels, Mutual Legal Assistance Treaties, bilateral information exchange, is a process measured in months. Informal networks and hawala channels leave no records in regulated systems at all.

AI-assisted investigation can work with the evidence that does exist domestically, following the trail as far as formal records allow, mapping the points at which funds cross jurisdictional boundaries, identifying the recipient-side entities through open source intelligence, beneficial ownership registries, and cross-referencing with known financial intelligence, building the most complete possible picture of where the trail leads even when not every step is directly documentable.

Sarvagata AI is built for this kind of multi-source investigative workflow. Agents can simultaneously process structured transaction data, query corporate ownership records, cross-reference financial intelligence databases, and integrate open source intelligence, including, when access is available, deep web and dark web financial communications. The integrated picture that emerges is more comprehensive than any single data source can produce, and it is produced at a fraction of the time that manual cross-source investigation requires.

Hawala and Informal Channel Detection

Hawala networks operate outside the formal financial system, no bank records, no transfer documentation, no institutional trail. They are among the most significant gaps in the formal AML monitoring architecture, and they are widely used in layering operations precisely because of that absence.

Detection relies on pattern recognition applied to the data points that do exist. Communication records that show coordination patterns consistent with hawala facilitation. Cash deposits and withdrawals on corresponding timescales across multiple unrelated accounts. Open source signals, forum communications, dark web references, that reference informal transfer activity.

AI analysis applied across these data types simultaneously can surface hawala-consistent patterns that would be invisible in any single data stream. No single signal is conclusive. The aggregate of consistent signals across multiple independent sources creates the evidential basis for investigation to follow.

Cryptocurrency Trail Reconstruction

Cryptocurrency’s role in layering operations has grown rapidly. The ED’s FY 2025–26 report identifies crypto-linked financial crime as a mainstream enforcement priority, no longer a niche concern. The ₹640 crore case referenced above, funds converted to cryptocurrency after passing through thousands of mule accounts, is representative of a pattern now appearing across multiple major enforcement actions.

Cryptocurrency trails are permanent and public on the blockchain, but they are not automatically readable. Address clusters, mixing services, chain-hopping across different assets, and peer-to-peer exchanges all create complexity in tracing that requires specific analytical capability.

AI-assisted blockchain analysis can trace transaction chains across wallets, identify addresses linked to known illicit activity or sanctioned entities, reconstruct the flow of funds through mixing services, and link on-chain activity to off-chain identities where exchange KYC data is available. This turns a trail that would be unnavigable without specialised tooling into a documentable evidence chain suitable for enforcement proceedings.

Continuous Monitoring, Not Case-Triggered Investigation

The most significant long-term shift that AI makes possible in AML investigation is the move from case-triggered to continuous analysis. Under the traditional model, investigation begins when a suspicious transaction is flagged or a case is opened. Everything prior to that trigger point must be reconstructed retrospectively.

Continuous AI-powered monitoring watches transaction patterns, entity behaviour, and network activity as it happens, flagging anomalies at the point they emerge rather than discovering them through retrospective reconstruction. When a pattern consistent with layering activity begins to form, the system surfaces it immediately. The investigation can begin at the point the trail is still warm, not months after the funds have been integrated.

This is the direction that the ED’s FY 2025–26 Annual Report points toward explicitly: regulators will increasingly expect continuous monitoring rather than periodic compliance reviews.

AML investigation involves some of the most sensitive financial intelligence a government or financial institution holds. Ongoing cases, source intelligence, STR data, and enforcement strategy cannot be processed on infrastructure outside the agency’s direct control.

Any AI system applied to this data must operate within the organisation’s own secure perimeter, on-premise, air-gapped where required, with no external data calls and no telemetry. This is not a preference for cautious agencies. It is the baseline requirement for deploying AI on data of this sensitivity.

Sarvagata AI‘s architecture is built around exactly this requirement. All models run locally. No data leaves the organisation’s boundary. Every investigation workflow, entity mapping, transaction tracing, pattern analysis, runs on the deploying agency’s own hardware.

To Conclude

The UNODC’s estimate that only 1% of global illicit financial flows are detected and seized is not an indictment of enforcement agencies. It is a measure of the structural gap between the complexity of modern money laundering and the capacity of manual investigation methods to close it.

The ₹81,422.63 crore in assets attached by the ED in a single financial year shows what determined enforcement can achieve. It also implies the scale of what remains, layering operations running across thousands of accounts and multiple jurisdictions, trails that currently require manual reconstruction over months, patterns that would surface immediately with AI-powered analysis applied across the full dataset.

Automated money trail analysis does not replace the investigator’s judgement. It removes the data assembly bottleneck that currently limits how deep that judgement can reach. The trails that are too complex to follow manually are not too complex for AI. They are just complex, and complexity, applied consistently and at scale, is exactly what AI is built to handle.

Frequently Asked Questions

1. What is money trail analysis in AML investigations?

Money trail analysis is the investigative process of tracing the flow of funds through financial transactions, from the point of origin in criminal activity, through the layering operations designed to obscure that origin, to the point of integration into legitimate economic activity. It involves mapping the entities and accounts through which funds move, identifying the beneficial owners at each stage, and building a documented evidence chain that meets the legal standard required for prosecution. In complex cases, this trail can span hundreds of accounts, multiple jurisdictions, and both formal financial channels and informal networks such as hawala.

2. How can AI automate money trail analysis?

AI can automate the most time-intensive stages of money trail analysis: automatically constructing entity relationship maps from transaction data, tracing fund flows across multiple accounts and jurisdictions simultaneously, identifying structural patterns in the network that indicate layering activity, cross-referencing across multiple data sources including corporate ownership records and open source intelligence, and surfacing hawala-consistent patterns across transaction and communication data. These processes, which can take weeks of manual investigation in complex cases, can be completed in hours by AI agents working across the full dataset in parallel.

3. Why is the layering stage of money laundering the hardest to investigate?

The layering stage is deliberately engineered to resist investigation. Funds move through multiple accounts, entities, and often jurisdictions in patterns designed to create complexity and distance from the original criminal act. Each hop is a transaction that may appear legitimate in isolation, it is only the pattern across many transactions that reveals the laundering structure. Manual investigation must trace each hop individually, which is time-intensive, scales poorly, and risks missing connections buried in the volume. AI-powered analysis processes the full transaction dataset simultaneously, rendering the complete network structure in a fraction of the time.

4. Can AI trace cryptocurrency in money laundering investigations?

Yes. Cryptocurrency transactions are permanently recorded on public blockchains and are traceable, but doing so requires specific analytical capability. AI-powered blockchain analysis can trace transaction chains across wallets, identify addresses linked to known illicit activity or sanctioned entities, reconstruct fund flows through mixing services and chain-hopping operations, and link on-chain activity to off-chain identities where exchange KYC data is available. This is increasingly important, the ED’s FY 2025-26 Annual Report identifies cryptocurrency-linked financial crime as a mainstream enforcement priority, and the ₹640 crore mule-account-to-crypto fraud case demonstrates the pattern now appearing across major enforcement actions.

5. What is continuous AML monitoring and how is it different from case-triggered investigation?

Traditional AML investigation is triggered by a report, a complaint, or a flagged transaction, and must reconstruct the money trail retrospectively from that point. Continuous monitoring uses AI to watch transaction patterns, entity behaviour, and network activity as it happens, flagging anomalies at the point they emerge rather than discovering them through retrospective reconstruction. When a pattern consistent with layering activity begins to form, continuous monitoring surfaces it immediately, allowing investigation to begin when the trail is current rather than after the funds have been integrated. The ED’s FY 2025-26 Annual Report explicitly signals that regulators will increasingly expect this shift from periodic to continuous monitoring.

6. What data sovereignty requirements apply to AI used for AML investigation?

AML investigation data, including STRs, ongoing case intelligence, enforcement strategy, and source intelligence, is among the most sensitive financial data a government agency or financial institution holds. Any AI system processing this data must operate within the organisation’s own secure perimeter, with no data routed through external servers, no cloud processing, and no telemetry. For enforcement agencies, this typically means on-premise, air-gapped deployment. For financial institutions, it means infrastructure that meets the RBI’s data localisation requirements and the organisation’s own information security framework. Commercial cloud-based AML tools that route investigation data through external systems do not meet this requirement.